This piece explains the key differences between third-party and comprehensive bike insurance through a real-world accident scenario in India

When you buy or renew bike insurance, you usually come across two main options: third-party bike insurance and comprehensive bike insurance. At first glance, the difference may seem simple. One costs less, while the other offers wider coverage. However, the actual impact becomes clear only when there is an accident, theft, fire, flood, or major repair expense.

Third-party insurance helps you meet the legal requirement and covers liabilities caused to another person, vehicle, or property. Comprehensive insurance offers wider protection by covering third-party liabilities as well as damage to your own bike. This is why choosing the right cover should not depend only on the premium. It should depend on how often you ride, the value of your bike, your repair cost exposure, and the level of financial protection you want.

Why is Bike Insurance Mandatory in India?

In India, every bike owner must have at least a valid third-party insurance policy to ride legally on public roads. This rule ensures that accident victims are financially protected. Riding without valid third-party insurance can lead to fines and legal consequences. For a first offence, the penalty can include a fine of ₹2,000 or imprisonment of up to three months, or both. For a subsequent offence, the fine can go up to ₹4,000, along with possible imprisonment.

However, having third-party insurance only means you are legally compliant. It does not mean your own bike is financially protected. If your bike is damaged in an accident, flood, fire, theft, or any other covered event, a basic third-party policy will not pay for those losses.

What Third-Party Insurance Actually Covers?

A Third-party bike insurance policy mainly covers your legal liability if your bike causes injury, death, or property damage to another person. For example, if your bike hits another vehicle and damages it, your third-party insurance can help cover the liability arising from that damage.

However, third-party bike insurance comes with a major limitation. It does not cover damage to your own bike. If your bike is damaged, stolen, burnt, or affected by floods, you will have to pay for the loss yourself. Third-party insurance also does not allow much customisation. You cannot usually add covers such as zero depreciation, engine protection, roadside assistance, or return to invoice with a basic third-party policy.

What Do You Get with a Comprehensive Cover?

Comprehensive bike insurance gives wider protection because it combines third-party liability cover with own-damage cover. This means it helps cover damage caused to another person as well as damage or loss involving your own bike. A comprehensive policy can protect your bike against accidents, theft, fire, natural disasters, man-made damages, and other covered risks. It also gives you the option to add extra covers depending on your riding needs.

For example, if your bike is damaged in a road accident, comprehensive insurance can help pay for repairs. If your bike is stolen, the policy can help compensate you based on the Insured Declared Value, or IDV, of the vehicle. If your bike is affected by flood or fire, the own-damage section of the policy can help reduce your financial burden. This is why comprehensive bike insurance is often preferred by riders who use their bikes regularly, own new or expensive bikes, or want better protection against sudden repair costs.

Third-Party vs Comprehensive Bike Insurance: Key Differences

| Basis of Comparison | Third-Party Bike Insurance | Comprehensive Bike Insurance |

| Legal status | Mandatory in India | Optional, but offers wider protection |

| Coverage | Covers third-party injury, death, and property damage | Covers third-party liability and damage to your own bike |

| Own bike damage | Not covered | Covered as per policy terms |

| Theft protection | Not covered | Covered |

| Fire and natural calamities | Not covered for own bike | Covered |

| Add-ons | Not usually available | Available with optional covers |

| Premium | Lower because coverage is limited | Higher because coverage is broader |

| IDV relevance | Not applicable for own-damage claim | Important for theft or total loss claim |

| Best suited for | Low-use or old bikes where only legal compliance is needed | Daily-use, new, expensive, or frequently ridden bikes |

This comparison also highlights why choosing the right bike insurance is not just about the premium, but about the level of protection you actually need on the road.

What Happens During an Accident?

The easiest way to understand the difference is through a real-world accident scenario. Suppose you skid on a wet road and your bike hits another vehicle. Both vehicles are damaged. If you have only third-party insurance, your policy can help cover the damage caused to the other vehicle. However, you will have to pay for repairing your own bike from your pocket.

If you have comprehensive insurance, your policy can help cover the damage caused to the other vehicle as well as the repair cost of your own bike, subject to policy terms, deductibles, and exclusions. This difference is important because even a minor accident can lead to repair bills involving body panels, lights, mirrors, brake parts, suspension components, or electrical systems. For newer bikes, these costs can add up quickly.

Why Premium Difference Should Not Be the Only Deciding Factor?

Third-party bike insurance usually costs less because it offers limited protection. The premium for third-party cover is regulated and is generally based on the engine capacity of the bike. Comprehensive bike insurance costs more because it includes both third-party liability and own-damage protection. The own-damage premium can depend on several factors. The premium depends on factors like the bike’s age, location, IDV, add-ons, and your claim history.

This is where many riders make mistakes. They compare only the premium amount and choose the cheapest policy without checking what they are giving up. A lower premium may save money during purchase or renewal, but it can become expensive later if your own bike gets damaged or stolen.

Why IDV Matters in Comprehensive Bike Insurance?

IDV stands for Insured Declared Value. It is the approximate current market value of your bike as declared in the policy. This value becomes important in cases such as theft or total loss. In simple terms, if your bike is stolen or damaged beyond repair, the insurer uses the IDV to determine the maximum claim amount payable, as per policy terms. IDV is not relevant in a basic third-party policy because that policy does not cover your own bike. It becomes important only when you have own-damage or comprehensive coverage.

Choosing an extremely low IDV just to reduce the premium may not always be a good idea. It can reduce your claim amount in case of theft or total loss. On the other hand, selecting a reasonable IDV helps you keep your coverage closer to the bike’s actual value.

What Add-ons Can You Get with Comprehensive Bike Insurance?

One major advantage of comprehensive bike insurance is the option to customise your policy with add-ons. These add-ons increase the premium, but they can be useful depending on your bike and riding habits. Riders can also enhance coverage with add-ons like zero depreciation, roadside assistance, or engine protection, depending on how and where the bike is used.

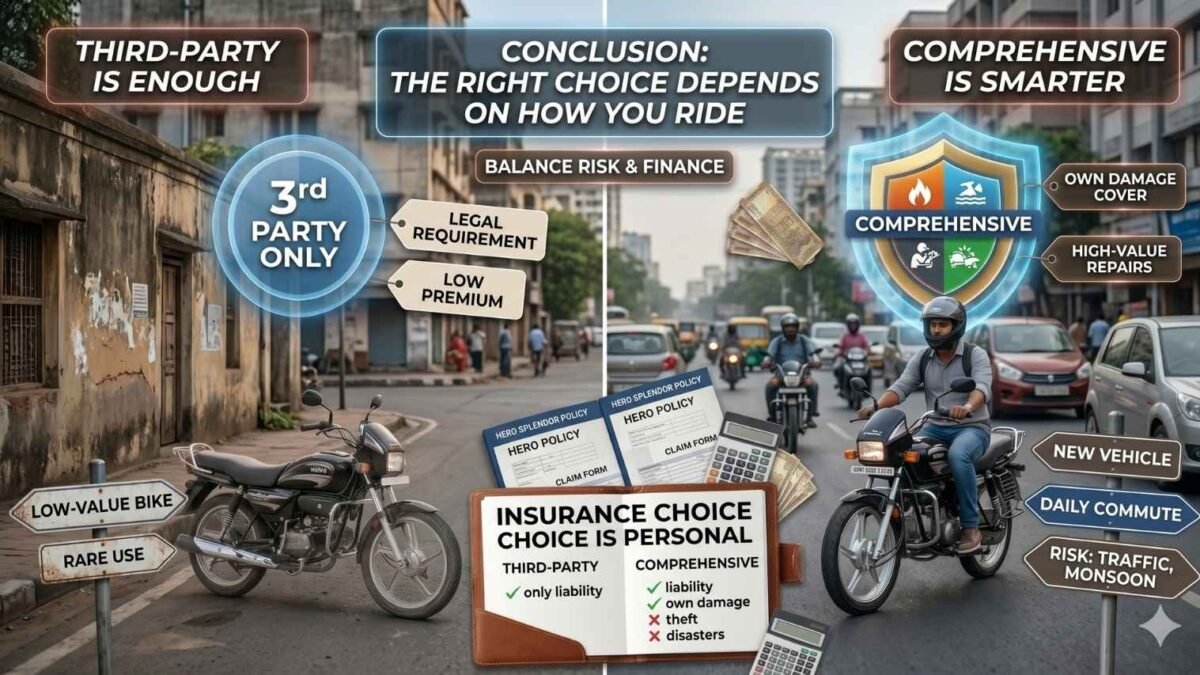

When Third-Party Insurance May Be Enough

Third-party bike insurance can be enough if you mainly want to meet the legal requirement and keep the premium low. It may also make sense if your bike is old, rarely used, or has a very low market value. For example, if you use your bike only occasionally and are comfortable bearing repair costs yourself, third-party insurance may be enough. It can also work for riders who have an older bike and do not want to spend much on wider coverage.

However, you must remember that third-party insurance will not cover your own bike. If your bike is damaged in an accident, stolen, burnt, or affected by floods, you will have to manage the loss yourself.

When Does a Comprehensive Cover Become Worth it?

Comprehensive bike insurance makes more sense if you ride your bike regularly, own a new bike, or depend on your two-wheeler for daily travel. It is also a better option if your bike has a higher market value or expensive spare parts. If you ride through traffic every day, minor accidents and road risks. During the monsoon, potholes, slippery roads, and waterlogging can further increase the risk of damage. In such cases, comprehensive insurance can help reduce the financial impact of repairs.

It can also be useful if you live in an area where theft risk, flooding, or accidental damage is a concern. Since the policy covers own damage along with third-party liability, it gives you wider protection in everyday riding situations.

Conclusion: The Right Choice Depends on How You Ride

There is no single bike insurance plan that suits every rider. Third-party insurance is the minimum legal requirement and helps cover liabilities caused to others. Comprehensive insurance offers wider protection by covering your own bike as well as third-party liabilities. If your bike is old, rarely used, and has a low market value, third-party insurance may be enough. However, if you use your bike regularly, own a new vehicle, or want protection against theft, accidents, fire, floods, and repair costs, comprehensive insurance is usually the smarter choice.

For most riders, the decision comes down to how much risk they are willing to take. Third-party insurance keeps you legally covered, while comprehensive cover protects your bike and your finances. If you rely on your bike daily, paying a slightly higher premium for better coverage often makes more sense in the long run.